>>> Δείτε τα αποτελέσματα στην Ελληνική <<<

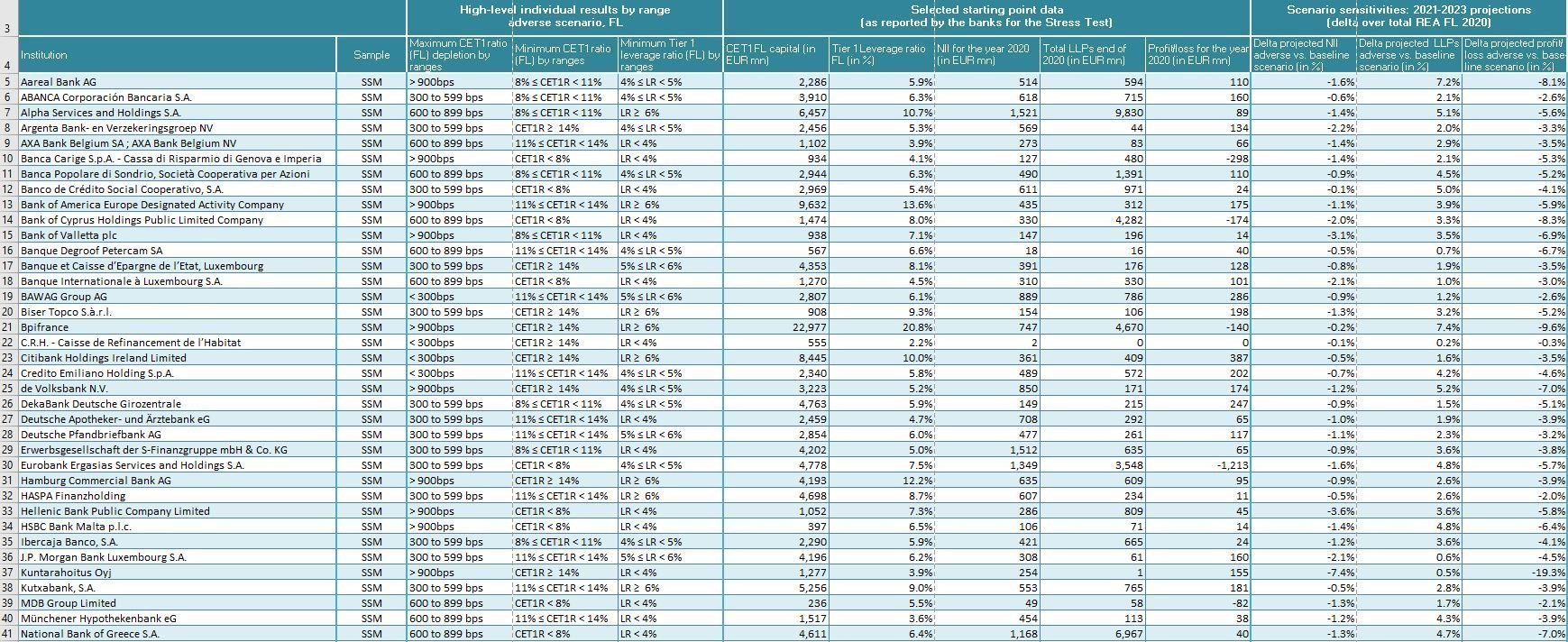

The European Banking Authority (EBA) published today the results of its 2021 EU-wide stress test, which involved 50 banks from 15 EU and EEA countries, covering 70% of the EU banking sector assets.

>>> Read results and info for Cyprus Bank, Hellenic Bank and RCB Bank here <<<

The aim of the EU-wide stress test is to assess the resilience of EU banks to a common set of adverse economic developments in order to identify potential risks, inform supervisory decisions and increase market discipline.

The EU-wide stress test is coordinated by the EBA and carried out in cooperation with the European Central Bank (ECB), the European Systemic Risk Board (ESRB), the European Commission (EC) and the Competent Authorities (CAs) from all relevant national jurisdictions.

This exercise allows to assess, in a consistent way, the resilience of EU banks over a three-year horizon under both a baseline and an adverse scenario, which is characterised by severe shocks taking into account the impact of the pandemic.

The individual bank results promote market discipline and are an input into the supervisory decision-making process. The adverse scenario has an impact of 485 bps on banks’ CET1 fully loaded capital ratio (497 bps on a transitional basis), leading to a 10.2% CET1 capital ratio at the end of 2023 (10.3% on a transitional basis).

Since the previous EBA EU-wide stress test in 2018, banks have continued building up their capital base, and at the beginning of the exercise (i.e. end-2020), had a CET1 ratio of 15% on a fully loaded basis (15.3% on a transitional basis), the highest since the EBA has been performing stress tests. This was achieved despite an unprecedented decline of the EU’s GDP and the first effects of the Covid-19 pandemic in 2020.

This year’s stress test is characterised by an adverse scenario that assumes a prolonged Covid-19 scenario in a “lower for longer” interest rate environment. With a cumulative drop in GDP over the three-year horizon by 3.6% in the EU, and a negative cumulative drop in the GDP of every member state, the 2021 adverse scenario is very severe, also having in mind the weaker macroeconomic starting point in 2020 as a result of the pandemic. The baseline scenario also provides some comparable information about individual banks in the context of a gradual exit from the pandemic.

Against this background, under the adverse scenario, the EU banking system as a whole would see its CET1 reduced by 485 bps on a fully loaded basis (497 bps on a transitional basis) after three years, while staying above 10%[1]. The results also show dispersion across banks. For instance, those banks more focused on domestic activities or with lower net interest income (NII), display a higher depletion.

>>> Read results and info for Cyprus Bank, Hellenic Bank and RCB Bank here <<<